Slim ,Tampa,Balboa,Stimpy and the rest of my frinds here YOUR Wrong! (not totaly but mostly) and your slaves to words

Its not bush or obama its all of the politicians

So, take a deep breath and put your reading glasses on (I have been working on this for a few days for yall.)

When someone gives you a check and the bank informs you that there are insufficient funds, who do you get mad at? In your own life, you get mad at the guy who gave you a check that bounced, not at the bank. But, in politics, you get mad at whoever tells you that there is no money.

One of the secrets of the growth of the welfare state is that politicians get a lot of mileage out of making promises, without setting aside enough money to fulfill those promises.

When Congress votes for all sorts of benefits, without voting for enough taxes to pay for them, they get the support of those who have been promised the benefits, without getting grief from the taxpayers. It's strictly win-win as far as the welfare-state politicians are concerned. But it is strictly lose-lose, big-time, for the country, as deficits skyrocket.

Anyone who says that we don't have the money to pay what was promised is accused of trying to destroy Social Security, Medicare or Obamacare-- or whatever other unfunded promises have been made. It is like blaming the bank for saying that the check bounced.

It is the same story at the state level as in Washington. The lavish pensions promised to members of public sector unions cannot continue to be paid because the money is just not there. But who are the unions mad at? Those who say that the money is not there.

How far short are the states? It varies from one state to another. It also varies with how large a rate of return the state gets on its investments with the inadequate amount of money that has been set aside to cover its promised pensions.

A front page story on the March 28th issue of Investor's Business Daily showed plainly, with bar graphs, how big mine and Tampas state; Florida's shortfall is under various rates of return on investments. Florida's own estimate of its pension fund's shortfall is based on assuming that they will receive a rate of return of 7.75 percent. But what if it turns out that they don't get that high a return?

A 6 percent rate of return would more than triple the size of Florida's unfunded liability for its employees' pension. The actual rate of return that Florida has received over the past decade has been only 2.6 percent. In other words, by simply assuming a far higher future rate of return on their investments than they have received in the past, Florida politicians can deceive the public as to how deep a hole the state's finances are in.

Political games like this are not confined to Florida. State budgets and federal budgets are not records of facts. They are projections based on assumptions. Just by manipulating a few assumptions, politicians can create a scenario that bears no resemblance to reality.

The "savings" to be made by instituting Obamacare is a product of this kind of manipulation of assumptions. Even when the people who turn out the budget projections do an honest job, they are working with the assumptions given to them by the politicians.

The fact that the end results carry the imprimatur of the Congressional Budget Office-- or of some comparable state agency or reputable private accounting firm-- means absolutely nothing.

When Florida arbitrarily assumes that it is going to get a future rate of return on its pension fund investment that is roughly three times what its past returns have been, that is the same nonsense as when the feds assume that Congress will cut half a billion dollars out of Medicare to finance ObamaCare. (Gov. Scott is trying to fix this and is catching hell from all ends for it.)

We would probably be better off if there were no Congressional Budget Office to lend its credibility to data based on hopelessly unrealistic assumptions fed to them by politicians.

One of the reasons why a federal "balanced budget" amendment is unlikely to do what many of its advocates claim is that a budget is just a plan for the future. It does not have to bear any resemblance to the realities of either the past or the future.

We do not need reassurances that do not reassure, whether these reassurances are in numbers or in words. No small part of the reason for the economic collapse we have been through is that federally designated rating agencies reassured investors that many mortgage-backed securities were safe, when they were not.

Not only investors, but the whole economy, would have been better off without these reassurances. "Caveat emptor" would be better advice for both investors and voters.

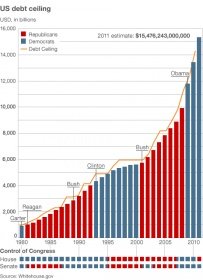

So we could definitely use another Abraham Lincoln to emancipate us all from being slaves to words. In the midst of a historic financial crisis of unprecedented government spending, and a national debt that outstrips even the debt accumulated by the reckless government spending of previous administration, we are still enthralled by words and ignoring realities.

President Barack Obama's constant talk about "millionaires and billionaires" needing to pay higher taxes would be a bad joke, if the consequences were not so serious. Even if the income tax rate were raised to 100 percent on millionaires and billionaires, it would still not cover the trillions of dollars the government is spending.

More fundamentally, tax rates-- whatever they are-- are just words on paper. Only the hard cash that comes in can cover government spending. History has shown repeatedly, under administrations of both political parties, that there is no automatic correlation between tax rates and tax revenues.

When the tax rate on the highest incomes was 73 percent in 1921, that brought in less tax revenue than after the tax rate was cut to 24 percent in 1925. Why? Because high tax rates that people don't actually pay do not bring in as much hard cash as lower tax rates that they do pay. That's not rocket science.

Then and now, people with the highest incomes have had the greatest flexibility as to where they will put their money. Buying tax-exempt bonds is just one of the many ways that "millionaires and billionaires" avoid paying hard cash to the government, no matter how high the tax rates go.

Most working people don't have the same options. Their taxes have been taken out of their paychecks before they get them.

Even more so today than in the 1920s, billions of dollars can be sent overseas electronically, almost instantaneously, to be invested in other countries-- creating jobs there, while millions of American are unemployed. That is a very high price to pay for class warfare rhetoric about taxing "millionaires and billionaires."

Make no mistake about it, that kind of rhetoric wins votes for political demagogues-- and votes are their bottom line. But that is totally different from saying that it will bring in more tax revenue to the government.

Time and again, at both state and federal levels, in the country and in other countries, tax rates and tax revenue have moved in opposite directions many times. After Maryland raised its tax rates on people making a million dollars a year, there were fewer such people living in Maryland-- and less tax revenue was collected from them.

In 2009, many people specializing in high finance in Britain relocated to Switzerland after the British government announced plans to take 51 percent of high incomes in taxes.

Conversely, reductions in tax rates can lead to more tax revenue being collected. After the capital gains tax rate was cut in the United States in 1997, the government collected nearly twice as much revenue from capital gains taxes in the next four years as in the previous four years.

Similar things have happened in India and in Iceland.

There is no automatic correlation between the direction in which tax rates move and the direction in which tax revenues move. Nor is this a new discovery.

Back in the 1920s, Secretary of the Treasury Andrew Mellon pointed out that people with high incomes were simply not paying the high tax rates that existed on paper, because they were putting their money into tax shelters.

After the tax rates were cut, as Mellon advocated, investments flowed back into the private economy, producing higher output, rising incomes, more tax revenue and more jobs. The annual unemployment rate in the next four years never exceeded 4.2 percent, and in one year was as low as 1.8 percent.

Despite political demagoguery about "tax cuts for the rich," in human terms the rich have less at stake than working people. Precisely because the rich have so many ways of avoiding taxes, a high tax rate is likely to do them far less harm than it does to the economy, on which millions of people depend for jobs.